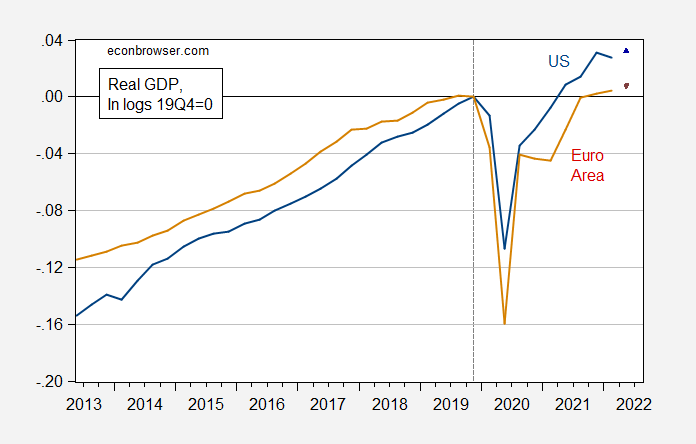

We now have first-quarter GDP for the US and the Eurozone. Although the US inflation rate measured by CPI/HICP is higher than the euro area (U.S. core has accelerated 0.7 percentage points relative to EA since the pandemic)the US GDP growth rate has also been high.

figure 1: U.S. real GDP (blue) and Eurozone 19 (brown), both expressed as the logarithm of 2019Q4=0. The 2022Q2 observation for the US is GDPNow (5/4) and the EA is Cascaldi-Garcia et al. (5/6). Source: BEA and Eurostat, via FRED, Atlanta Fed, Cascaldi Garcia, Ferreira, Giinone and Moduñoand the authors’ calculations.

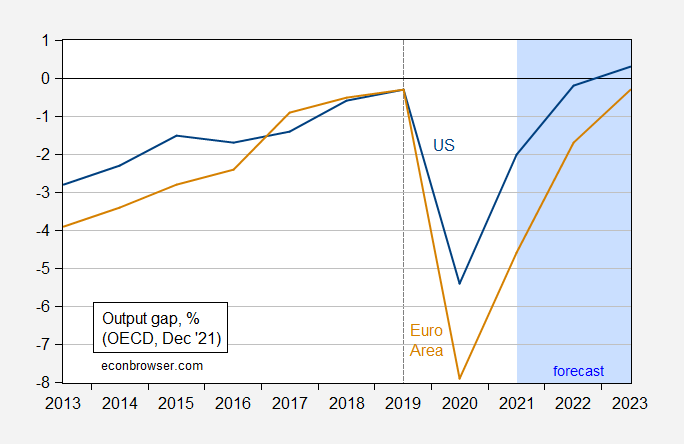

Since growth is constrained by potential or full employment GDP in the long run, it is not meaningful to make differential comparisons of growth before and after the pandemic.However, we can see if the US output gap is closing faster than the euro (remember It is important to note that the output gap is very difficult to measure).

figure 2: US output gap (blue), Eurozone 17 (brown), %. Light brown shading indicates predictions. Source: OECD.

This means that over the three-year period 2020-22, the cumulative output gap between the US and East Asia is 6.6 percentage points of GDP.

It is worth noting that the output gap measures the deviation of output from potential GDP and does not directly include cost-push shocks – so if these estimates are to be believed, the acceleration in inflation is not primarily due to demand-pull (relative to potential) .

{kind=link}

{kind=link}