This is the week for the small fry. Those of us who don’t have savings accounts with $250,000 in them, and don’t have to worry about big corporate payroll cash, get to celebrate that we avoided a scare as some regional banks started to collapse like dominos, with investors and CFOs looking around in some panic to try to guess who might be next. Sometimes “too small to worry” is almost as good as “too big to fail.”

In terms of investments, though, it’s probably time for the big guys. When the world is in a panic, we’ve seen that the money leaves the small banks and rushes into the perceived safety of JP Morgan and Bank of America, regardless of how much those giant banks are screwing their depositors (and boosting their own profits) by offering absurdly low savings account yields. And likewise, when the markets are jittery, it’s the stocks that are big and relatively stable, and the companies who don’t depend on anyone else to fund their operations, who tend to attract money. When things are scary, investors tend to want to invest with companies who don’t need their money. Small caps had their moment in January, but it might be over already… at least for a little while.

Lots of readers have written in to ask what on earth is going on with the banks, and what they should do, so I’ll try to answer some of those questions in a general way (I can’t tell you what to do with your money, of course, I’m not your financial advisor and have no idea what your situation might be… and if I gave you personal advice, the SEC would be on me like a ton of bricks). If you can’t stand to read one more thing about the bank crisis, rest assured that my insight and blather is probably not uniquely valuable… you can just skim down to the next **** if you want to skip it.

The first wave of questions came last weekend, and they were essentially answered before the market opened on Monday — lots of readers asked what would become of Roku (ROKU), because that happened to be the tech company that had the most money (and the largest percentage of its cash, about 25%) tied up in an uninsured Silicon Valley Bank (SVB Financial (SIVB)) account. There were a lot of company names thrown about on Friday that had a lot of cash tied up at SVB, including Roblox (RBLX), but the only one I noticed that was more exposed than Roku was tiny AcuityAds (AT.TO, ACUIF), which had something like 90% of its cash at that bank. I watched AcuityAds for quite some time after the Motley Fool teased it as being “maybe another Trade Desk (TTD)” because it was trying to launch a new ad buying platform, but they’ve so far not been able to fulfill that promise in any real way, or even grow their revenue, so I haven’t seen a reason to invest… but one of the things they have going for them is a good chunk of cash left over from some equity raises in recent years, especially relative to their small size (they have about $60 billion in cash, market cap $85 billion), so anything that threw that cash into question was a real crisis for AcuityAds, and apparently close to $50 billion of their cash was in uninsured accounts at SIVB. They had a rough weekend.

But as of Sunday night, that worry disappeared for Roku and AcuityAds and everyone else. All deposits of any amount at SIVB and Signature Bank (SBNY) became effectively “insured” by the FDIC as those banks were closed down by the regulators, and were available to those depositors — if not instantaneously, then at least quickly. In the end, no pain for the companies that got perhaps a bit too careless with the corporate treasury… the pain was reserved for shareholders in those banks, their management teams and employees, and maybe the companies who lent those banks money (that will shake out over a much longer period of time, SIVB just declared bankruptcy to start the process).

Behavior is likely to change, however. Believe me, CFO’s everywhere have been scrambling to fix this problem for the past week, now that bank safety is a clear risk that investors will ask about and hold them responsible for, and that will probably continue to be something investors and management teams talk about and prepare for over the next couple years. Everyone is eager to close the barn door, now that they feel bad about their neighbor losing his horse and are worried it might happen to them.

Which means, of course, that although we’re going to hear talk about this on quarterly conference calls for a little while, and investors will be fretting over whether this rescue from the Feds is a “bailout” for risky corporate behavior, and whether a couple more banks might fail if the crisis of confidence spreads, we can be pretty sure that the next crisis will be something completely different. For me, the core issue is that the inverted yield curve means the borrow short/lend long business, which is really the core of banking (take deposits, which can be recalled at any moment, and use them to lend money for 5-30 years), is an awful business right now, mostly because of the Federal Reserve’s push to stop inflation by raising short-term interest rates to levels far above the long-term rates that we all got used to. And it’s such a bad business that the impact will probably reverberate across the economy, since banking and similar ‘carry trade’ levered investments are really at the heart of so many businesses.

Those artificially low long-term rates (and low inflation) became an implied “this is normal and will always be this way” part of the financial world over the past decade or so, built on the fact that we hadn’t seen persistent inflation for 30-40 years, and that really warped the thinking of investors, gradually but perniciously (including me, I’m sure). There are a lot of businesses that just don’t make any sense at even half their current price if the 10-year Treasury Note goes to 6% and stays there, and many of them can adjust, over time, if interest rates normalize… but some can’t or won’t.

And as an extension to that, all of the relatively low-return “non-correlated” businesses that form a lot of the foundation of the economy and are extremely dependent on cheap debt, like commercial real estate, are also at risk of being pretty lousy businesses right now… especially if their funding has any cracks in it (like, if they depend on public shareholders buying more shares of REITs, or on constantly rolling over short-term debt). Commercial mortgages often have to be refinanced every five years, and are generally non-amortizing (meaning the principal is not paid back over time, like your mortgage is), and the only reason people bid the prices of office buildings up to having low cash yields (5% or less, sometimes much less at the peak) is because they could borrow at 2-3% and thought they could raise rents in perpetuity.

Commercial mortgages that come due this year are certainly not being refinanced at 3%, and might have to be refinanced at 6% or 8% if the building is in any trouble or has a high vacancy rate, which means the building will lose money unless they can raise rents, and if it’s an office building whose tenants are downsizing because they’re sticking with a partial work-from-home strategy, or just becoming more cost-conscious, they can’t raise the rents that much without dropping occupancy further and making the building even less profitable. That’s why we’re seeing a wave of office building mortgages defaulting — buildings that a private equity firm or insurance company were happy to buy at a 5% cash yield to diversify their portfolio and provide some “hard asset” exposure five years ago now look stupid because they’re no longer full, and the cost of borrowing the money to continue to own those buildings is rising, so, like the homeowners who got scammed into mortgages they couldn’t afford in 2006, and ended up owing a lot more on the mortgage than the property was worth in the open market, those building owners are mailing the keys back to the bank and giving up the hope that their equity in the property has any value. I don’t know if this is the third inning of feeling this ripple in the economy, or the eighth inning, since I’m apparently legally obligated to use baseball metaphors if I want to talk about the economy, and I don’t know how bad it might get, but as the world comes around to realizing that these rate dynamics are not necessarily going to be short-lived, and as the bank crisis scares everyone a little more, it’s obviously a worrisome time for any business that relies on the persistent availability of cheap debt. Or, like commercial real estate, relies on the big regional banks. We’re really not going to know which companies are managing this scary environment well, with hedging or other tools, until it’s probably too late to do much about it (Warren Buffett once said, “You don’t find out who’s been swimming naked until the tide goes out” — he was talking about the rising competition from Bermuda reinsurance companies at the time, that quote is from the 1994 Annual Meeting, but the same dynamic applies throughout the economy right now… cheap and easy debt got so built into so many businesses, for so long, that we stopped thinking about it for a while, and that era seems to have ended).

That’s just one example, the impact of cheap money and low interest rates has seeped into lots of cracks in the economy, slowly, over decades, and now that we’re about a year into this era of rapidly rising interest rates and still-strong inflation, expectations about going back to “normal” have gradually gotten much less optimistic over the past six months or so, and those cracks are beginning to widen. That’s why inverted yield curves (long-term rates lower than short-term rates) are a sign of a coming recession — the Fed is the final source of “money” in the economy, I guess, but in our system most money is really created by banks making loans. Now things have tightened enough that banks are likely to be more careful with their lending, or in some cases (like these faltering regional banks) might not have the capacity to lend, and rates are climbing fast enough that people are worried about borrowing, and that can slow the economy down much faster than the Fed raising its overnight interest rates. The Savings & Loan Crisis of the late 1970s and early 1980s, which led to big federal rescues and scandal and roughly 10% of banks eventually failing over the following decade or so (mostly small banks, so not 10% of the banking sector, 10% in number of banks), was essentially caused by rising interest rates and inflation, too (there were also regulatory screwups, so I’m oversimplifying).

If we’re lucky, this bank-driven tightening helps to squash inflation more quickly, the Fed can “normalize” rates relatively soon, and we have a relatively long period of stagnation or mild recession, because risk-taking is quieted for a while and everyone sits back and licks their wounds. If we’re not lucky, then the unease over banks spreads as a contagion to unease over many other sectors of the economy, stock market multiples come way down as bonds become reasonable investments again, real estate crashes, and we have a long bear market while everything resets. That may well also cause even more political unrest, if inflation sticks around and unemployment picks up, I just hope it doesn’t fan the flames of the Ukraine war or the Taiwan standoff and spread those fires. A bad economy tends to make people want to fight.

Those are not the only scenarios, of course, it’s always possible that we stumble along and everything works out fine — despite what we would like to believe, the economy is not an engine that we can tinker with and predict with any certainty, it’s just a big bowl of people and emotion and unintended consequences and complex relationships.

So we got a bank run spreading from a little fella (Silvergate and its risky cryptocurrency business) to some very large banks (Silicon Valley Bank was one of the 20 largest banks in the US), and threatening to spread to many other large regional banks… and that’s good news? The market seemed relieved about it to open the week, partly because the government stepped in to extend FDIC insurance to all deposits… but probably mostly because this mini-crisis, one dreams, might be enough to get the Fed to stop hiking interest rates, finally giving investors what they really want: A return to wild speculation and a refilling of the punch bowl, and, really, a hope that we’re going to go back to the low interest rates on which so many businesses and “financialized assets” (like commercial real estate) depend.

And having Credit Suisse, one of the largest global banks, again remind us that it has been a crisis-in-waiting for a decade provided some more worry about the stability of the global financial system. They quickly got access to some rescue lending from the Swiss government, but even that potential crisis, much larger in scale than these few US bank failures so far, also seemed to be a tonic for some stocks. Big tech stocks, in particular, celebrated the banking panic (the Nasdaq 100 and gold were both up about 5% this week)… not because it’s good for them that Silicon Valley Bank’s turmoil is causing a crisis among startups, or because even the Saudis won’t put more money into Credit Suisse, but because all this turmoil means investors are again hoping that the Fed will get more “dovish” on interest rates, even if inflation isn’t falling as quickly as hoped. And for most of the most popular stocks, the Fed is still the story. That will probably be next week’s obsession, as we await the Federal Open Market Committee’s press conference and next interest rate announcement (on Wednesday).

I’m not deeply involved in banking, and generally am not smart enough to understand the income statements or balance sheets of the big banks, which is why I don’t buy those stocks… but you don’t need me for that, every investor on Twitter is now a banking expert (they’re flexible, they were experts on epidemiology a couple years ago, and on Eastern European politics last year), so you can find someone to back up whatever opinion you might have, but my favorite articles about this crisis have been from Matt Levine at Bloomberg… here’s an excerpt from one of them earlier in the week (“SVB Took the Wrong Risks”):

“It is, I think, fair to say that Silicon Valley Bank took some bad risks, and that’s why it ended up failing. It is a bit harder to say exactly what SVB’s bad decision was. A simple answer is “it made a huge bet on interest rates staying low, which most prudent banks would not have done, and it blew up.” Yesterday Bloomberg reported that “in late 2020, the firm’s asset-liability committee received an internal recommendation to buy shorter-term bonds as more deposits flowed in,” to reduce its duration risk, but that would have reduced earnings, and so “executives balked” and “continued to plow cash into higher-yielding assets.” They took imprudent duration risk, ignored objections, and it blew them up.

“I think that answer is fine. A more complicated answer would be that they took duration risk, as banks generally do, but their real sin was having a concentrated set of depositors who were uninsured, quick-moving, well-informed, herd-like and very rates-sensitive in their own businesses: If all of your money is demand deposits from tech startups who will withdraw it at the slightest sign of trouble and/or higher rates, you should not be investing it in long-term bonds. This is a more subtle answer than “just hedge your rate risk bro,” and it is arguably more understandable that SVB’s executives would get it wrong, but in any case it certainly ended up being a bad risk.”

And thanks to the internet, and the financial media, and everyone being a little bit edgy after the past couple years of stress, one run on a bank begets a couple more runs, and maybe some banks whose businesses or mistakes were similar, if not as extreme, also end up being closed down, though it’s clear that the FDIC and the government are planning to make sure depositors are saved. Which makes sense, there is an argument to be made that rich people and corporations should be careful about where they keep their excess cash, and that the risk of money being uninsured should mean that those folks are extra careful in choosing their banking partners, which enforces discipline on the banks… but really, the financial system works best for everyone if we generally have a world where you don’t have to worry about your bank deposits, no matter how big they are (if that sentiment fails, then pretty soon the big-four banks, or the big-six, get ALL the cash deposits, don’t have to compete, and we lose what little innovation, customer service or competition there is in the banking industry). Personally, I don’t really care about the “moral hazard” of saving excess deposits, I don’t think we should expect a company that’s just trying to make sure they can meet their $300,000 monthly payroll to also be expert at assessing how much risk their bank is taking (even analysts miss a lot of this risk, and that’s their only job).

We haven’t had any bank failures in a year and a half, and haven’t had big ones in more than a decade, so perhaps folks like Roku who had hundreds of millions of dollars on deposit at Silicon Valley Bank were being foolish, I can see why those outliers look like idiots in retrospect, and maybe it would have been worth making them wait for their money while the FDIC cleaned up the mess, and even end up losing some portion of it in the end (probably a smallish portion)… but Roku and AcuityAds were the extreme exception among public companies (lots of unprofitable venture-funded startups were more extreme, with all their cash at SIVB, but we don’t know much about them), and Silicon Valley Bank itself was in many ways an exception, since they attracted big uninsured deposits from startup companies partly because they incentivized those companies to hold their cash at SVB in order to get the rest of their VIP banking relationship (jumbo mortgages for employees and other loans for executives, cash management for their venture capital funders, etc.), and because Silicon Valley Bank was truly entwined in the venture capital and startup world and considered part of the foundation of that economy. Nobody thinks the foundation is about to fail… until the earthquake hits, and suddenly everyone thinks about the foundation at the same time.

So what do we do? Other than stop watching CNBC, I mean, that’s definitely step one — their “crisis” coverage ramps up instantly to some combination of Election Night returns and Bernard Shaw reporting from under a desk during the aerial bombing of Baghdad in 1991. I’m surprised they didn’t have “BANKS IN CRISIS 2023” hats made up for the anchors to wear.

Well, for me the first step is “don’t get tempted to buy banks.” Many of them are cheap and still very profitable right now, and sharp price drops are always tempting, but they’re mostly lousy businesses in this environment, and I’m not going to be the guy who tries to nimbly buy some beleaguered regional bank on a down-30% day and sell back for a 20% gain a week later. If you’re a trader, these are pretty exciting times in financials, but I don’t have the stomach for that.

I ended up writing several notes about the crisis in the comments to an older bank stock pitch, mostly because that pitch (teasing TFS Financial (TFSL), from Tim Melvin) continued to circulate last week, as Silicon Valley Bank was beginning its collapse. Melvin rightly pointed out that most banks are much more effectively managed than SVB was, particularly when it comes to hedging the risk of a long-dated bond portfolio in a world where interest rates are spiking higher… but I think he still skates over the risks to bank profitability during this kind of interest rate shakeup. More on that in a minute.

There are two reasons why people go through the hassle of pulling their money out of their regular bank — which is really all a bank run is, it’s too many people pulling out their money, too fast, something NO bank can handle: First, they are worried that the bank will fail… or Second, they are getting a lousy interest rate compared to other available bank accounts, or otherwise getting a lousy product or service.

The first risk is being pretty effectively dealt with, it seems to me, even for companies and wealthy individuals who have more than the FDIC-insured $250,000 in any given bank account. The FDIC and the Federal Reserve have done away with the insured account limit at those two failed banks in order to save those deposit bases and stop uninsured depositors everywhere else from panicking. We’ll see if the rules really change, there has been no permanent lifting of the FDIC insurance limits for other banks… but the limit on FDIC insurance has been tested, and it has been found lacking. If the next bank failure means some company’s payroll account is suddenly frozen on a Friday afternoon, the Feds have shown us that they’ll step in. You know, probably.

It seems to me that we should probably require FDIC insurance for all bank deposits, no matter the size, and scale the FDIC insurance premiums that banks pay, or make big depositors pay the insurance themselves. That’s effectively what we already do with the “too big to fail” banks — if something insane happens and Citibank or JP Morgan or Wells Fargo is about to go under, you know that they would be bailed out and rescued, probably not just their depositors but also the banks themselves and, at least to some degree, their shareholders, no matter how much that might stink… the global economy can’t handle a collapse of those banks, therefore every deposit is effectively insured at those banks, and no company will ever be criticized for depending on Citibank or JP Morgan.

Those mega-banks “pay” for this by facing extra regulatory scrutiny, and in return they get to collect massive deposits and face no real competitive pressure to pay higher yields on those deposits. As long as that’s the situation, then all you’re doing by enforcing FDIC limits is saying that every bank that’s not too big to fail has to live under the limits… which means that every CFO in America will move their accounts to one of the biggest banks, therefore wounding the regional and local banks who do most of the lending, and further increasing borrowing costs for regular businesses. And all of those regional banks are run by people who have a lot of clout in their local city or region, are often the largest business in a given town, and sit at the head table at fundraising dinners for their Representatives and Senators.

The second risk, though, is what is probably beginning to hurt smaller banks more right now. Most banks don’t have a ton of uninsured large deposits that might flee in a hurry, and in that way SIVB and a few other banks that specialize in corporate accounts and the uber-wealthy (or flighty industries, like unprofitable startups or cryptocurrencies) were farther out on a limb. But most non-gigantic banks are facing much more competition for deposits than was true the last time interest rates went up in a meaningful way… and therefore they face the risk of a slow-motion “run” on deposits that erodes their capital base and cuts into their profitability. If those banks rely heavily on large portfolios of long-term bonds without a lot of interest rate hedging, like 10-30 year Treasuries or mortgage bonds, like SIVB, then losing any meaningful amount of deposits to competitors is a big deal… because they can’t afford to sell those bonds at a stiff loss, and some of these smaller banks can’t afford to pay higher rates on deposits. They’re stuck with portfolios of bonds which seemed sensible a year or two or three years ago but that now yield much less than the most competitive savings accounts. Many banks might not even really be able to afford to borrow from the Federal Reserve at 4.5%, because even that is much higher than the yield they’re earning on the long-term fixed-rate mortgages they hold.

The Feds are making it a little easier to handle those underwater bonds and mortgages that many banks own right now… as part of this stem-the-crisis response, they’re offering to lend money based on the par value of securities (so they’ll lend you money based on the $1,000 par value of that fixed-rate 30 year mortgage bond that has 29 years left to pay, even if they market value of that bond is down to $800 now because interest rates have shot higher), so that might effectively rescue a lot of smaller savings banks that hold lots of mortgages on their books… but it won’t necessarily rescue their profits, it will just help them remain solvent. That strikes me as a pretty good balance — I think government intervention to save depositors is reasonable, there’s a definite benefit from that for the economy, but we don’t want the actual banks and their management and shareholders to profit from any mismanagement that might appear in their income statement.

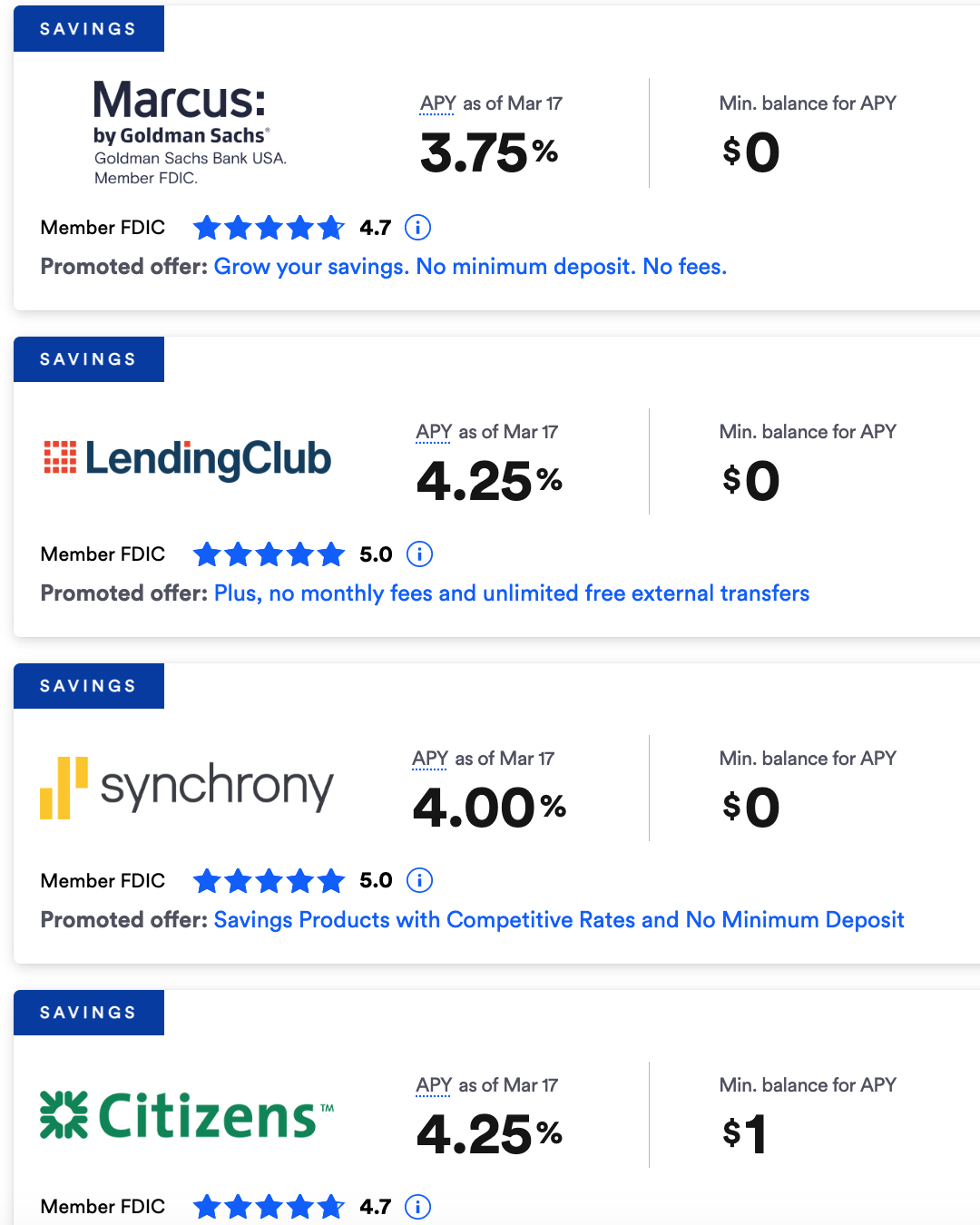

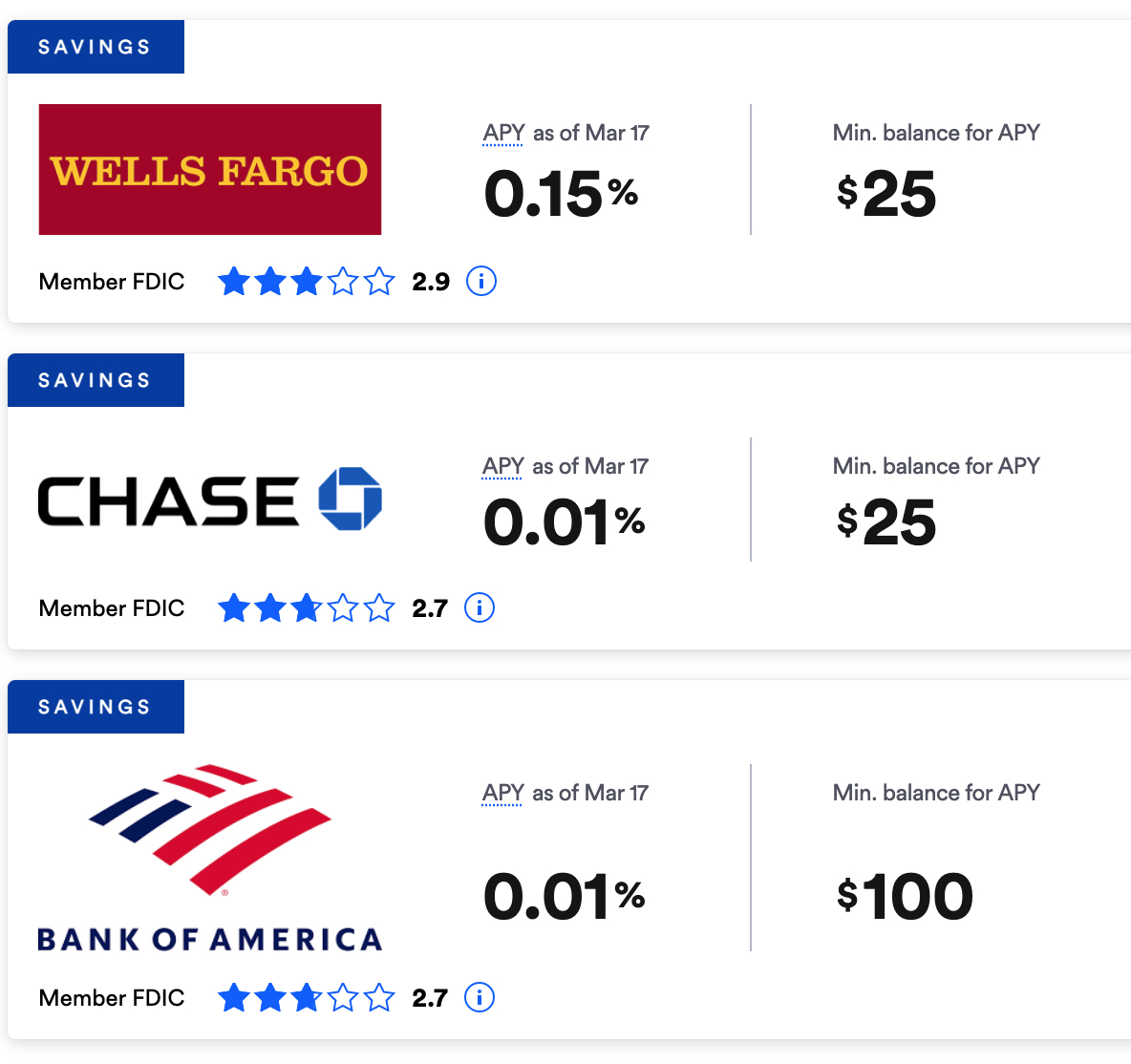

Speaking of the banks that have those implicit guarantees, though? The ones that are sure they don’t have to worry about losing customers? Just check out the rates that were offered on savings accounts earlier this week — this page is from Bankrate.com:

Look at those smug bastards… Wells Fargo, Chase, Bank of America… don’t tell me that they’re not benefitting from “too big to fail” or the implicit government guarantee for the mega-banks, that’s downright insulting. 0.01%, for God’s sake, who the hell can get away with that?! All they have to do is collect those deposits from people who are now afraid of smaller banks, put them into T-bills yielding 4%, and lean back in their chairs and light their cigars. It’s a good week to be Jamie Dimon.

TFS Financial (TFSL) can’t get away with that, that’s for sure — I’m not picking on them, a lot of banks are in a similar position, that just happens to be the bank I was writing about in recent months because Tim Melvin has been teasing it as his favorite high-yield bank stock, so it’s one of the few banks where I’ve looked in detail at the numbers. And I gather it may be a fairly extreme example of the squeeze some small banks are seeing. These are the yields being offered by more aggressive banks right now:

Last I saw, TFSL’s bank, Third Federal Savings and Loan, is now offering three-month CDs that pay 3.5% (4% if you tie it up for three or four years), and it seems inevitable that they’ll be raising their offer on regular old savings accounts (currently they say they pay 1%). They should have to, as a small bank, otherwise the money will flow out the door — either to the perceived safety of a mega-bank, since giving up a 1% yield isn’t so hard to do if you’re worried about bank solvency, or to a bank that offers a competitive yield for deposits, with many now offering 4-5%. There is often a lot of loyalty to a local bank, and certainly a lot of friction that keeps people from moving banks, but if you’re being offered 4% or 5% then you’ll feel like a chump for settling for 1%, especially if that 1% yield doesn’t come with the safety of a mega-bank. People generally don’t accept chump-hood in perpetuity.

I did see this offer that someone on Twitter received — don’t know if it’s real or not, or if it was a test or widespread, but it’s the kind of thing we should expect to see.

$TFSL starving for deposits. Not a good sign. pic.twitter.com/ma1akoYTaC

— Five Putts (@fourputtjojo) March 9, 2023

TFSL makes about 3-3.5% on its mortgage portfolio, most of which is 30-year mortgages that are nowhere near maturity, and their cost of borrowing, both from loans and from deposits, has been 1.5-2%, but is going to ramp up much more quickly than their income from the mortgages.

Does that mean there will be a “run” on TFSL? Are they going to collapse? No, not necessarily. They have a balanced portfolio to some degree, there are some adjustable rate mortgages, and they do make new mortgage loans that will help offset some of the new higher rates they’ll have to pay, it’s not instant… and interest rates have been dropping this week, which might help if that continues. What it really means to me is they’re at risk of making a lot less money, not that they’re necessarily at risk of being in a crisis or suffering a bank run in the near future. Especially with that new Fed backstop offering to lend them money at par value for those 30-year mortgages they’re stuck with.

So we won’t necessarily end up with a lot of bank runs, as long as Jerome Powell and Janet Yellen can reassure people that the fires have been put out… but when short-term rates go up dramatically, the banks who rely on very long-term assets (10+ year bonds and 30-year mortgages) and who finance those long-term assets with short-term deposits, are walking a tightrope. That’s what banking is, there’s always that mismatch between assets and liabilities… but the mismatch doesn’t usually get highlighted so dramatically, because the yield curve is usually not so dramatically inverted (with short term rates higher than long-term rates). You can take a chance on regional banks and small banks, they’ll probably bounce back if the rate picture normalizes in the next six months, and the Feds seem quite committed to halting contagion in the banking industry and making sure they get out in front of any “bank run” behavior, but I don’t see a lot of appeal in buying any banks right now.

If I were looking for yield in the banking sector, I’d consider the preferreds of any of the mega-banks before I considered buying into small thrifts or regional banks — those beaten-down smaller banks might be fine, but reading a bank balance sheet and getting any confidence at all about how much risk they’re taking is almost impossible for normal human beings like me. And the mega banks, as long as they keep paying 0.01% on the deposits that are rushing in their doors right now, are going to be just fine, which means that the discount preferred stocks that are trading now, priced below their $25 par value and yielding 5-6% in most cases, should be very safe. They might not do great if inflation stays at 5-6% for a long time, but they’ll pay their dividend and most will probably recover to $25 eventually.

Then again, maybe this mini-crisis in the banking sector has reset the Federal Reserve, again, and the Feds will stop raising interest rates, instead relying on prayer (or crossing their fingers) to get inflation back down, and maybe we’ll be lucky and the long-lag effect of the jump from 0% to 5% in the Fed Funds rate will kill off inflation by the end of the year, even without more rate hikes. That was the bet earlier this week, when several pundits and analysts began to insist that if the inverted yield curve was killing banks… the Fed would have to stop inverting the yield curve, pulling back from that possible 0.5% increase in rates that we all expected to come next week, or from a potential 6%+ terminal rate that scares everybody, and maybe instead they’ll be cutting rates in the next few months.

Indeed, in some ways Wall Street has that angry toddler vibe going again — “if you keep hurting the stock market and raising interest rates, we’re going to hold our breath and stomp on the floor until we break the economy!” We’ll see how firm Mama Yellen and Papa Powell are as the angry toddler picks up steam. If the Fed does not follow through on the widely expected interest rate hike next week, then Wall Street wins and nobody will believe the Fed when they say they’re tough on inflation. Which will bring a sigh of relief for banks and tech stocks, but would also probably be bad news for the dollar, and good news for gold.

But I wouldn’t bet on traditional banks. They look pretty cheap, and in many cases they might be fine, but no matter how you look at it, paying 4% to depositors to finance loans that you made at 3% is a lousy business, and you have to be pretty confident in your prognostications about the future to buy a lousy business. I don’t know what happens over the next six months, so I’ll generally try to focus on companies that I think are good businesses… or at least have a clear path to becoming good businesses in the future, without being completely reliant on whatever the Fed Funds Rate might happen to be between now and August.

The one thing we can be pretty sure of? The big banks are likely to get massively stronger, even if that’s not what anybody really wants to see happen — they can pay much less for deposits, they will never be allowed to fail, and they don’t have to compete. Every single company and wealthy person is thinking about moving their liquid capital accounts to one of the largest banks right now, even if they don’t really need to because they’re under the $250K legal limit and their regional bank or local bank is probably fine and their deposit definitely insured. During times of rising tension, and gossip about “who’s next,” there’s no value in “probably fine.” Either it’s fully guaranteed and too big to fail and you’re sure there will never be a liquidity crisis at your bank, or you’re not sure. In times of crisis the world becomes black and white… “safe” is seen by many as worth the cost of the 2% or 4% returns that you could get from “probably safe” … especially if you’re worried that your family or your shareholders or your employees are going to ask you why your stock is crashing, or why your payroll checks didn’t clear, or why the check to the kids’ private school bounced.

If I were in a position where I had $250,000 or more in demand deposits, or even something a bit less than that if I had to access the money instantly (sometimes FDIC insurance takes a day or two to kick in after a failure), I would spread them out.

If you’re worried about the limits, which some readers have also asked about recently, do also note that the limit of $250,000 is not absolute — it’s per person, per institution (that oversimplifies a bit, but it’s the safest way to think about it). So if you’re married, and you and your spouse have a joint savings account and a checking account, $500,000 in total across those accounts at a single bank would be FDIC insured. Anything more than that, assuming it’s not in a different kind of ownership structure like an IRA or a trust account, might be uninsured at that bank. I would consider that to be perfectly safe, but sometimes having a belt and suspenders is more reassuring, so if I had that much in liquid savings that I wanted easy access to, Imight split it among two or three banks. Especially if I needed it to be available instantly (like if you’re in the process of buying a home and have to close in a few weeks, for example, or have a big tuition bill due for your triplets at Harvard). There probably won’t be a bank run at your bank, and you’d get your money back pretty quickly even if there was, but who knows, maybe the bank’s website goes down for a day when you need it, or your account gets screwed up and you have to argue with customer service on a weekend, it’s nice to have more than one bank account even if you don’t technically need it under the FDIC insurance rules.

But doubling or tripling your insurance coverage is incredibly easy… just open accounts at one or two more banks, which will only take a few minutes. Your insured deposit at JP Morgan has no relation to your insured deposit at Bank of Boca Raton, you can easily have $250,000 insured at each bank, per person.

If you’re in an even more fantastic tax bracket, and have well over $250,000 that you want to be insured under one name, with the best rates you can get, there are also some services that will make managing this glorious headache much easier — they’ll break up those deposits for you and manage that, for a (hopefully) small fee. Maxmyinterest.com is one of those, they don’t hold custody of your money but they offer you a dashboard and let you move your money around to various accounts to get the best rate and make sure it’s all insured and easy to keep track of, and they charge something less than 0.2% per year — that probably wasn’t worthwhile when everyone was paying less than 1% on deposits, but now it seems pretty reasonable if it makes it more likely that you’ll pull your savings from JP Morgan at 0.01% and get 5% from FDIC-insured accounts elsewhere. (There are other services like this, too, that’s just one that I’ve looked at in the past).

Brokerage cash accounts are different, to be clear — they are insured, too, but they’re insured by the SIPC, which effectively offers $500,000 in coverage for an individual brokerage account, up to half of which can be cash… so that covers your brokerage cash account, as well as custody of any regular securities you own (which includes things that are not quite cash, like money market mutual funds — there are exceptions, some annuities and limited partnerships are not covered, for example). In effect, if you have $250,000 in cash in a brokerage account, that, too, is insured against the failure of the brokerage firm, very similar to how the FDIC insures you against the failure of your bank. (To be clear, the SIPC does not insure against stocks or investment losing value — just against your brokerage firm failing and putting your custody of those assets in any kind of limbo). In actuality, many brokerage firms (all the big ones I’ve ever looked at) offer insurance coverage beyond the SIPC limits, just to provide investors with a little more peace of mind, so most people are effectively covered for well over a million dollars — and even beyond that, the risk of several of your investments falling by 100% is much, much higher than the risk of ever losing the stocks and funds you own because your brokerage goes out of business. In a world awash in worry, this is one thing I don’t personally worry about.

*****

But that’s all big picture and banking stuff, and while we do need to know what’s going on, and we need to worry a little bit about the impact on the economy, we’re not going to be able to predict how it turns out. So let’s step back and talk about our investments for a minute.

What am I worried about? Well, as inflation stays persistent I’m pretty worried about highly-levered companies with tight profit margins, and I’m also a bit worried that commercial real estate might be a really rough business for the next several years, as it gradually resets for a world where interest rates stay higher for longer than we previously guessed.

Largely for that reason, I decided today to finally sell my position in Kennedy Wilson (KW), which is an excellent property developer and owner of a lot of profitable and stabilized properties in the Western US and Europe (Ireland and the UK), with good insider ownership and a small but pretty strong asset-management business that has grown quickly in the past few years. It’s still a good company, and they have hedged their borrowing exposure for the moment (their effective borrowing rate is now only a little over 4%, and the average term is five years or so, which gives them a lot of flexibility), so this is not necessarily a disaster in the making, and they do have some really profitable multi-family developments in Washington and Idaho that could continue to produce steady cash flow, (well, as long as everyone isn’t forced to go back to Seattle and San Francisco and show up in an office every day, at least)… but even with that low-cost debt, they’re not making much money, and they depend on being able to sell new developments to reinvest into other projects, which might be challenging in this environment.

In many ways, Kennedy-Wilson acts like a REIT, with the valuation partly based on its dividend yield (5.5% today), but it carries a lot more debt than a REIT would be allowed to have. That was good a few years ago, and is less good now. I just think it’s a risk I don’t need to be taking, while I’m already quite exposed to levered real estate through the much larger and more diversified Brookfield (BN and BAM)… I should have sold last year, when I started to be a little worried about them, but the multi-family portfolio has been doing well, and that kept me holding on. I no longer think that’s worth the risk.

Brookfield Corp (BN) is in some ways riskier than Kennedy Wilson, because of its exposure to probably the most dangerously overpriced commercial real estate in recent years, the big office towers and prime shopping malls owned by Brookfield Property, which account for roughly half of Brookfield Corp’s assets, (Kennedy Wilson’s office exposure is generally more suburban, and smaller as a percent of their assets)… but Brookfield also makes dramatically more money on its asset management business, which continues to attract capital, and trades at a huge discount to the book value of those properties. Brookfield investors are already assuming that those properties will be terrible, and I think it’s likely that they’re probably discounting them too much (partly because many of these are real “trophy” assets that should hold up even if overall vacancy rates rise), but that discount gives us some wiggle room. Brookfield also has market heft that will get it better terms than most property investors, hundreds of billions of dollars of investors’ money that earn them a steady management fee (and is either permanent capital, or locked up for a long time), and a much longer track record of compounding value for shareholders… along, of course, with the fact that the other half of Brookfield’s business, outside of real estate, is largely focused on communications and electricity infrastructure, green energy, and distressed debt, all high-growth areas that are less sensitive to interest rates. I wouldn’t bet on either of these companies having a fantastic 2023, and they may well both work out OK over a longer period of time, but I’m much more confident in Brookfield’s long-term prospects. I’m interested in reducing some of my exposure to debt-driven real estate, and will do so by jettisoning Kennedy Wilson. I’ll let you know if my thinking changes on that in the future. That ends up clearing the Real Money Portfolio at $16.91 per share, which is a tiny profit but really mostly just means I broke even on that position over a few years… not a great success, in the end.

*****

And I also increased my position in a relative new holding this week, with an add-on buy of Huntington Ingalls Industries (HII) shares, which is basically an annuity on the aircraft carrier fleet of the United States (yes, that’s an exaggeration… but an easy shorthand way of thinking of HII). The Federal budget is a shambles, and we may well see politicians fighting over everything, even possibly restricting the defense aid to Ukraine at some point, but one thing everyone agrees on is that we have to worry about China… and confronting China and helping Taiwan and otherwise projecting US force around the world as a balance to China’s expansive goals depends on having a strong Navy, built around big carrier groups and nuclear submarines, the two main businesses at HII’s shipyards. HII is not going to grow fast, but neither is it likely to see much loss of business in the next 50 years, as aircraft carrier orders and maintenance should be steady and their exposure to the expanding nuclear submarine fleet grows, and they’re currently in good shape as they catch up with some inflationary challenges in their shipyards (including finding workers) and continue to clean up their balance sheet, so I think there’s a good chance that the company will look much better, and earn a higher multiple, at some point over the next several years.

I effectively doubled my stake in HII this week, through a series of purchases between $206 and $200 as the stock fell. The valuation has now come down to about 12X forward earnings, with a dividend yield that’s slowly becoming meaningful (it’s about 2.5% right now, but the dividend has grown steadily, doubling over the past six years).

I don’t actually really love owning weapons makers, that’s not the world I’d like to see growing over the next decade, but it’s hard to see an industry that is more likely to be resilient in the near future than defense. I’m also still actively considering some of the other big players in the space, including Northrop Grumman (NOC), which is Huntington’s former parent (they were spun out in 2011), as well as supplier Curtiss-Wright (CW) and EU leader Leonardo (LDO.MI, FINMF or FINMY), though haven’t “pulled the trigger” on any other defense positions. I wrote about a bunch of those a few weeks ago, in case you missed it.

*****

Other news?

I gave up on Illumina (ILMN) a while back, mostly because the hullabaloo (and massive cost) of their re-acquisition of Grail was screwing up a fundamentally excellent leading oligopoly in the genetic testing space. The core business of selling DNA sequencers and selling the test kits and services around those machines is excellent… the company’s results in recent years, not so much, other than the boost they got for COVID testing work.

And now Carl Icahn is stepping in, trying to force change and threatening to run a proxy campaign to replace three of Illumina’s board members, mostly because he says Illumina’s re-acquisition of Grail was a massive management blunder that cost shareholders ~$50 billion. I think he’s right, but we’ll see how it plays out.

Frankly, this makes me think that maybe I should just buy some Icahn Enterprises (IEP), the odds are pretty good that Illumina will take Icahn seriously (I already have call options on IEP)… the risk there, for me, is that Carl Icahn is the second-oldest and arguably second-most-influential investor in the US, and he’s much more pugnacious and active than number one (Warren Buffett is 92, Carl Icahn is 87). That doesn’t necessarily mean Icahn won’t be fighting with entrenched corporate executives ten years from now, he’s a pretty unique guy… but it seems to me that his battles must be more stressful and tiring than Warren Buffett’s, and I wouldn’t have the energy for that (I’m 52, in case you’re wondering). Who knows, maybe it’s the fights that keep him young, but presumably Icahn’s family will be running IEP whenever he decides to step down (he owns roughly 80% of the partnership, and in effect is gradually taking it private by reinvesting his dividends), and I don’t know anything about his successors, or about whether the culture and strategy at Icahn Enterprises can survive the inevitable change of leadership (that will be a challenge for Berkshire when Buffett leaves as well, though I’m more confident in the persistent culture and strategy at Berkshire).

I do think that IEP is likely to have a very strong year or two as the market tries to reset to some rationality in a world of higher interest rates, and Carl Icahn can slap companies into being sensible better than almost anyone else. He’s also one of the few big investors who remembers what it was like when inflation and interest rates spiked in the 1970s, and has always had an eye for distressed debt, so there’s a good chance he’ll get some big “wins” in this kind of market. But his age and my lack of understanding of who’s standing behind Icahn at Icahn Enterprises keeps me from making a meaningful equity commitment at this point, even with what is currently a tempting 15% dividend yield for his publicly traded partnership. I’ll continue to think about it and research the situation, but for now I’ll just continue to bet on Icahn having a big year or two with my small call option speculation (because investors have grown accustomed to thinking that the big dividend yield is the only thing IEP can provide, expectations of the share price rising are quite low, which means options are pretty cheap — I own the January 2025 $55 call options, which are essentially just a bet that IEP is likely to have at least a 10%+ share price boost at some point… they did so in 2007, 2012 and 2018, we’ll see if it happens again).

*****

And we got a good non-banking question this week from a reader, so I thought I’d chime in on that… here’s the question:

“You got my attention on Kinsale Capital last month just before the 30pt boost following the earnings call. I have been following the stock closely since. I notice some large declines in the past two weeks as to the stock value. I was wondering what size portfolio they manage and if there is a correlation to the managed assets and the decline in the companies stock price. I live within 2 miles of Markel’s home office; but, I had never heard of Kinsale Capital until I read your update on the company last month.

Lastly, Since becoming a paying member of the “Gumshoe” I have enjoyed immensely going back reading all Friday reviews for 2022!”

First of all, thanks for joining us as a paying member! It really helps.

As regards Kinsale Capital (KNSL) and whether the stock is driven by its investment portfolio, the answer is “not really” — they do have a growing portfolio of investments, mostly investment-grade bonds, so that portfolio value will fluctuate, but it’s still teensy in comparison to the company’s market capitalization. Kinsale has an equity portfolio (mostly just ETFs) that’s worth something in the neighborhood of $100 million, and they have a total of about $2 billion in cash/short term investments (like Treasury Bills) and another $2 billion in long-term investments, which would include that $100 million in equity but would mostly be longer-term corporate and government bonds. The cash is essentially a backstop for the unearned premiums and the reserve for unpaid losses, which are roughly in that same $2 billion neighborhood.

That means rising rates could hurt a little bit in their long-term bond portfolio, even if they’re likely to hold all of those bonds through to maturity (as many insurance companies do, including Markel), but rising short-term rates will also dramatically increase the cash yield from their short-term investments, with 3-6 month T-bills often yielding 4% or more recently. And more importantly, that long-term portfolio isn’t a big enough “tail” to really wag the Kinsale “dog”.

Kinsale is much more of a “are earnings sustainable” story than a “what will the portfolio be worth” story. They have a market cap of about $7 billion, and an investment portfolio of about $2 billion. Markel, in contrast, has a market cap of about $17 billion, and they have $18 billion in cash and short-term investments, which (like Kinsale) roughly covers their $18 billion in unpaid loss reserves and unearned premiums, but Markel also has a $22 billion long-term investment portfolio, with a pretty high allocation to equities within that portfolio (roughly a third of that is likely in equities at the moment). This is oversimplifying, but you can kind of imagine that a $1,200 share of Markel is being driven in a pretty meaningful way by about $1,550 in investments per share, while a $285 share of Kinsale is not nearly as influenced by about $80 in investments per share.

That will probably evolve over time, Kinsale’s portfolio is likely to grow as they continue to write more profitable insurance and compound the company’s value, but it will take quite a long time for the portfolio to become the tail that wags the dog, as sometimes is the case with Markel. Most traditional insurance companies are closer to Markel than to Kinsale in this regard, their portfolios are large enough to drive their results when interest rates shift, though they often also pay out meaningful dividends instead of trying to compound their book value (Markel, emulating Berkshire, reinvests its profits instead of paying out dividends), and they rarely are as aggressie as Markel has usually been in allocating a large part of their portfolio to equities or, in the case of Markel Ventures, wholly owned non-insurance businesses.

In general, rising interest rates are a good thing for insurance companies — it can cause short-term pain in the long-term bond portfolio, but these companies specialize in managing interest rate risks over decades and match their liabilities to the assets, which lets them hold the bonds to maturity even if they have to write down the value, and the benefits of being able to invest their next dollar at higher rates quickly make up for that unless they make some big portfolio mistakes. Inflation, on the other hand, is not so good — it does give them room to raise rates, which is good, the property and casualty market has generally been in a “hard market” with insurance prices going up for several years, but it also raises the payouts for insured losses, and therefore means the insurance companies have to reserve more for potential or likely claims.

I think Kinsale’s relative weakness is mostly a function of being a very richly valued stock — it gets traded like a high-growth stock, not like a regular insurance company. I still am very wary of Kinsale… it doesn’t make sense to me that they can consistently be this much better than their competition at underwriting specialty insurance, generating huge underwriting profits, and being that different is a caution flag that the competition should wise up and improve at some point. But I do keep holding, because right now they ARE that much wildly better than the competition, and they’ve kept up that outperformance for years, continually surprising analysts and investors with how much money they’re making (even without a real investment portfolio)… so maybe they really do have some special secret sauce that’s hard to compete with in their niche underwriting areas. Some companies are just much better than others, and we don’t want to sell them just because it’s hard to understand why they’re better.

{kind=link}

{kind=link}